Curriculum

Tips to manage money

Introduction

0/1Part 1: Learn the basics

0/7-

1. If you don't know the problem, you can't find the solution.

Preview

Preview -

2. Don't spend more than you have.

Preview

-

3. Today's debt = spending tomorrow's income

Preview

-

4. Carry only what you can bear.

Preview

-

5. Focus on what matters.

Preview

-

6. Don't walk blindfolded: plan!

Preview

-

7. Planning a little is better than not planning at all

Preview

Part 2: Let's go further

0/6Part 3: the world of finance

0/77. Planning a little is better than not planning at all

We can’t plan everything…but not planning makes all your expenses become emergencies: planning a little is better than not planning at all.

How is your budget coming together? Is the jigsaw puzzle taking shape? Don’t walk blindfolded… open your eyes to see obstacles. Not so easy? If planning and budgeting were super easy, everybody would do it. What are the main reasons why many of us don’t budget?

- Budgeting is…depressing: there are too many expenses and too little income! Well, writing a budget does not make your expenses bigger and your income smaller; budgeting just shows your income and expenses in bright light, all together, so that you can prioritise your expenses, save for future ones and fit them all in your income. If you spend without planning, are you really setting your priorities… or are the shops setting them for you? Maybe your income is irregular… unlike your rent which is depressingly the same amount every month. Budgeting forces to tackle the potential shortfalls before they happen… with a cool mind, very much like reviewing your lessons before an exam. Once you get used to budgeting, you will find that NOT budgeting is stressful, because problems happen and you have hardly any time to find a solution. Not planning makes all your expenses become emergencies. So don’t be hard on yourself: plan all you can reasonably plan.

- A budget is too many numbers: experiment… and try to find the tool that you are comfortable with (see lesson 6 “practise”). Fine-tune your categories of expenses: if there are too many, that makes a lot of numbers. Choose the level of detail which is significant and easy to plan and add up.

We can’t plan it all anyway

Planning a little is better than not planning at all. Look at your expenses from last month (you’ve got them all thanks to your notes): how many could you have planned? Rent, food, bills… should be relatively easy to plan. But how can we manage real emergencies like health expenses, damage to your home, accidents, something broken in your bike?

- Prevent: maybe you can’t plan, but you can try to minimise these emergencies: take care of yourself and whom and what you are in charge with: eat moderately and eat good food/drink safe water (sometimes it is more expensive… but good nutrition will help you stay fit); exercise your body and your mind; sleep well; keep a good hygiene (wash your hands, teeth…); pay attention when you drive, relax, feel grateful, have a fulfilling and active family, social and spiritual life… all this helps keep fit for the long term and minimise the health bills; … manage your money to avoid unnecessary stress; maintain your bike, house, etc… to minimise big repairs and include these maintenance expenses in your budget.

- Save for emergencies: how much did you spend on real emergencies in average over the last months? Include that amount in your budget – this will force you to re-prioritise your expenses: maybe cut down on going out for example, to save a bit for a potential emergency. If the emergency does not incur, all the best: you can keep these savings for future emergencies… or use them for another important purpose, like helping a family member, or spend on any prevention tool like buying a padlock for your bike, etc… If the emergency happens, you will be less stressed as you have thought of a financial solution already.

- Insure: inquire about insurance possibilities…

More on insurance

Life is risky, and sometimes risks are just too big for one person to bear: huge medical expenses due to an illness or an injury, loss or damage in property (fire, flood, theft…), or loss of income due to a permanent or temporary disability for example; that’s where insurance can help.

- Public national insurance: some countries have free or subsidised public healthcare systems, generally financed by compulsory contributions paid by employers and employees. Check what exists in your country.

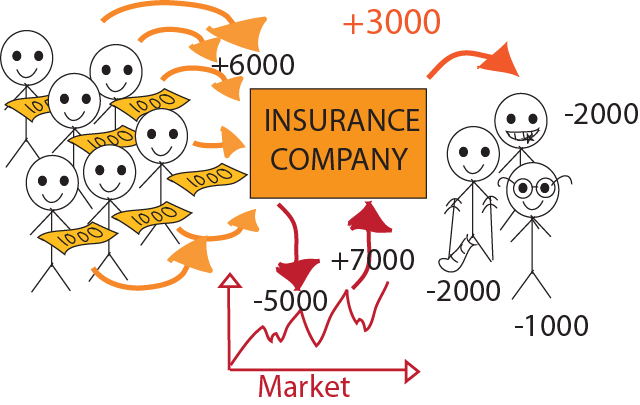

- Private for-profit insurance companies: you sign an agreement with an insurance company: you pay an amount called “premium” every year or month and they will pay for the costs of the risk if it happens. What are the money flows?

- Lots of people sign agreements with the insurance company, and pay premiums. If the risk happens to one of the insured persons, the insurance company takes from the “pool” of premiums and pays the cost. Insurance companies are for profit businesses: they calculate the probability of risks and how much it would cost. For example, based on historical statistics, 20% of their 10,000 customers may have a tooth decay that costs $100 to cure, so a total cost of $200,000, plus the company’s administrative expenses and profit, let’s say $250,000 that they split between the 10,000 insured people (or “policyholders”); in this super simplified example, the premium that each insured would pays would be $25.

- The insurance company gets the premiums once a year or month and will have to pay back or pay the hospital directly once in a while when the customers actually experience the covered risk and declare it to the insurance company. Do all these collected premiums sit in the insurance company’s bank account ? No, the insurance company tries to get additional revenues by investing the premiums.

- What happens if you pay a health insurance and never get sick? The bright side is that it is nicer to be healthy than sick. The premiums you paid over the years were used to pay for other insured customers’ expenses, the insurance company’s administrative expenses… and profit for its owners. A premium is an expense… not an investment.

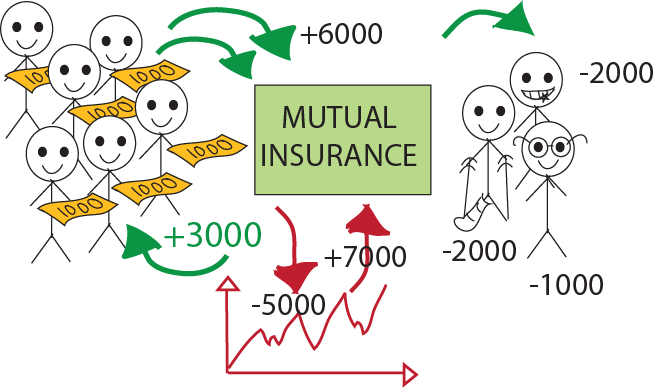

- Mutual insurance companies/associations:

The main difference with a for-profit insurance company is the ownership: customers are also the owners of the association or company. So every year, they approve the accounts and discuss what to do with the profit (or loss): keep it to cover future risks, or share it usually by reducing next year’s premiums (or increasing them if losses).

How to choose?

- Some insurances are compulsory: for example, in many countries, you need a vehicle insurance to drive. Check your country’s requirements.

- It is about future expenses… and we don’t know the future; it all depends on your risk assessment: think about the risks you / your family may face and what you consider you could cover by yourself (“self-insurance) and what you could not. For example if your family has no eyes’ issues history, why take an insurance that will cover glasses and opticians?

- Compare: various insurance providers that can cover the risks you have identified. Read very carefully:

- what risks are covered and under what conditions: you don’t want to pay a premium… and realise that the risk you thought was covered is not covered. For example, losses from floods are covered, except for agriculture revenue or if you live less than 100 meters from a river. And you own cattle that graze on your field next to the river),

- who are covered in your family,

- how much it costs (premiums) and how much you still have to pay out of your pocket (the insurance will usually ask you to still pay an amount (“deductible”) or a percentage (“co-payment)”: for example, for any medical consultation, you have to pay $50 and the insurance pays the remaining cost).Include the premiums and emergency savings in your budget and re-prioritise the other expenses. It is a trade-off: usually the more you pay out of your pocket (“higher deductible” in insurance language), the lower the premium will be. The big question to ask yourself is how much risk you are ready to cover?

- And whether you prefer using a for-profit or a mutual insurance.

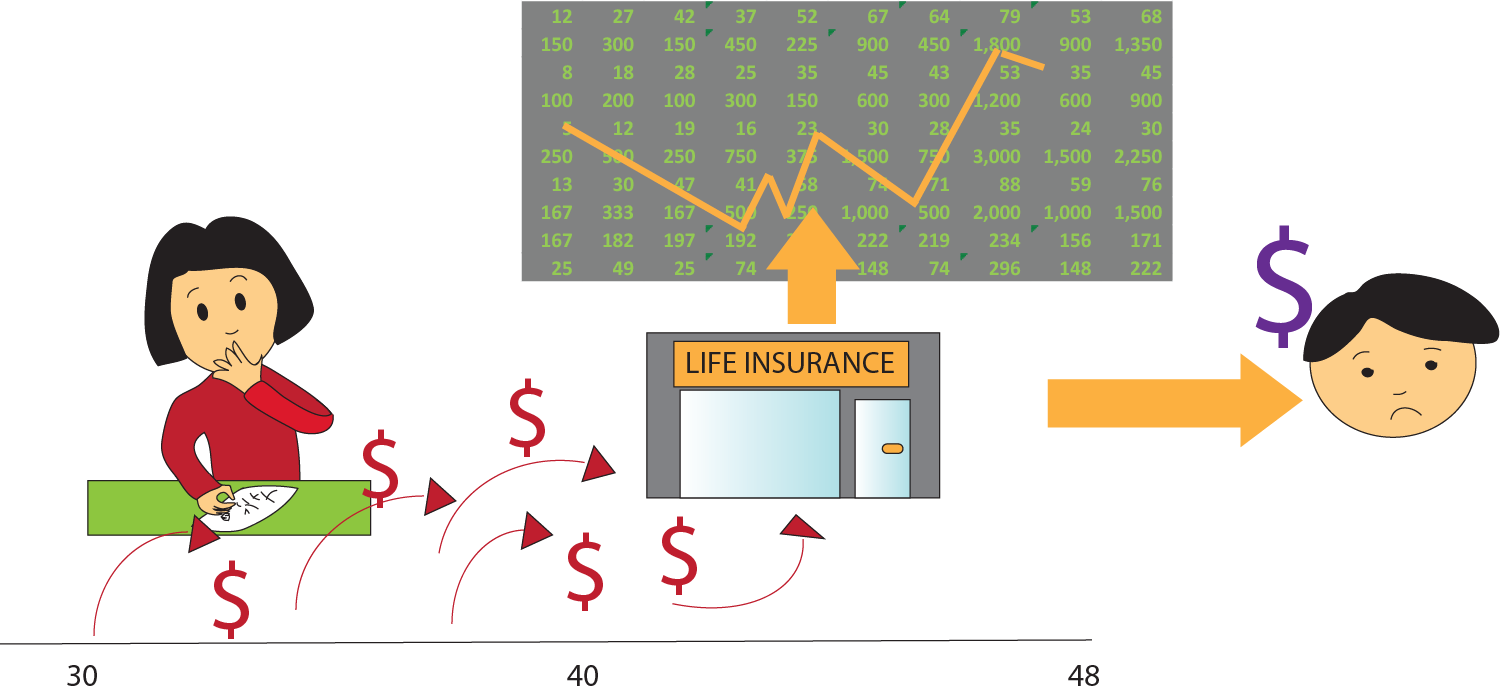

What about life insurance? There are two main types:

- Real life insurance:

- You pay a premium every month to the insurance company.

- If you die, the insurance company pays a lump sum to your beneficiaries.

- Usually people take that kind of insurance when they still have children at charge.

- If you decide to stop the insurance (for example, you retire and can’t pay the monthly premium any longer), you don’t get any money back – this is an insurance, not an investment.

- The insurance company invests the premiums and gets an income from these investments and generally makes a profit on premiums: it receives more premiums than it pays lump sums because in some contracts, people pay the premiums but stop before dying so the company does not pay anything).

- Before subscribing or not this type of insurance, think about what could happen to your loved ones after your death, especially if you are the main breadwinner: can a family member take care of your children, do you have valuable assets that could be sold to pay the tuition for your children, etc … and even more important: are all your papers in order? Will your family will not be unduly dispossessed because documents proving you own your home for example are missing?

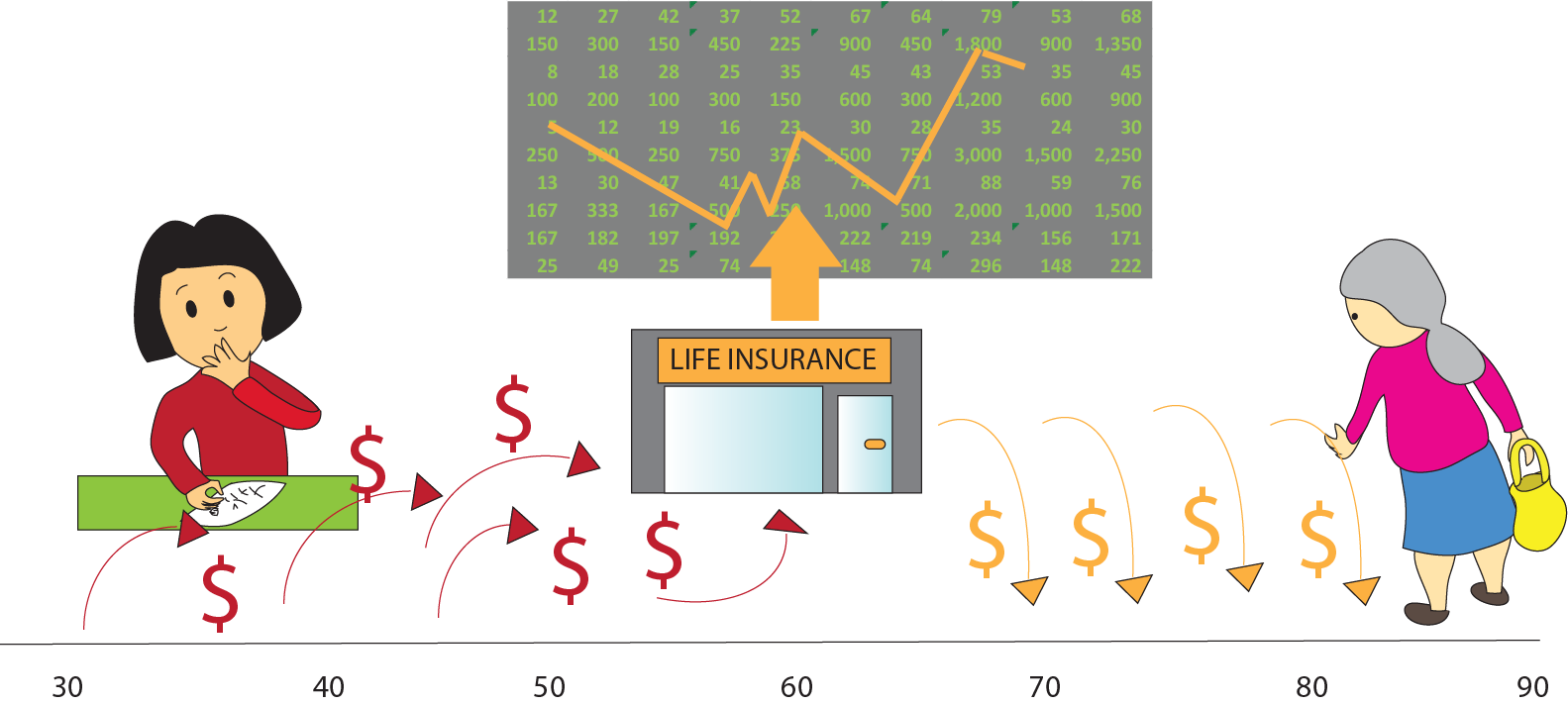

- Life insurance as investment:

- You pay a premium every month to the insurance company.

- At some point in time, the insurance company pays either a big lump sum or an annuity (yearly payment) until you die.

- It is a long term investment and the insurer’s fees are usually high.

- If your life circumstances change over time, you may have to stop policy and take new one (or not any) ; it is usually hard to change the policy details (standard products).

- Always do some calculations: take several scenarios (with different life expectations), and compare the total premiums to pay vs. the expected benefits; is it worth it? Have you got other ways to prepare for your retirement?

Let’s put this into practice:

- Prevent: Take a close look at your life style: are you taking care of yourself? Are you taking care of whom and what you are in charge with?

- Save: look at your actual expenses and compare them to what you had budgeted: how much have you not planned last month: are they likely to happen again? If they are, include them in your budget. If some expenses were real emergencies, include an amount in your monthly savings goals.

- Insure: read further then inquire and compare insurance possibilities, ask questions (don’t sign up for something you don’t understand) and consider taking what makes sense to you (and not to the insurer or the broker…). Don’t over-insure yourself.

Take your time and read this lesson several times. Inquire and ask questions. Don’t sign if you don’t understand or under pressure.

Planning a little is better than not planning at all. If you don’t plan, all your expenses become emergencies! Increase your well-being and peace of mind by planning – and free your mind to focus on what matters.