Curriculum

Tips to manage money

Introduction

0/1Part 1: Learn the basics

0/7Part 2: Let's go further

0/6Part 3: the world of finance

0/7-

14. Savings: questions to ask yourself

Preview

Preview -

15. Money is not mysterious

Preview

-

16. Investing: what are the flows?Sorry, this lesson is currently locked. You need to complete "15. Money is not mysterious" before accessing it.

Preview

-

17. Main investmentsSorry, this lesson is currently locked. You need to complete "15. Money is not mysterious" before accessing it.

Preview

-

18. ⚠️ Beware of scams

Preview

-

Two more important points

Preview

-

Your action planSorry, this lesson is currently locked. You need to complete "Part 2: Let's go further" before accessing it.

Preview

15. Money is not mysterious

Have you written down your savings goals? Have you categorised them as short-term, medium-term, and long-term?

Let’s take a closer look at how money flows when we save or invest. Looking at money as a flow helps us think where it comes from and where it goes… and hopefully makes money look less mysterious… even what looks very mysterious to many of us: savings and investing. As you read further, note down your questions: does that make sense to you? Have your goals with you and ask yourself which type of savings/ investments could be relevant to each of your goals. In this lesson, we are focusing on savings.

Savings at home:

In this case, there is no flow of money. The money no longer circulates; it stays at home, with the risk that you might use it for something else, that it might be stolen, or damaged (fire, flood, pests, etc.).

| Pros | Cons |

|

|

Keep the minimum amount of cash you need and leave the rest in the bank or your mobile money account. Keep this cash in the safest place possible (hidden, locked away, etc.). Count it and regularly check that it matches your tracking.

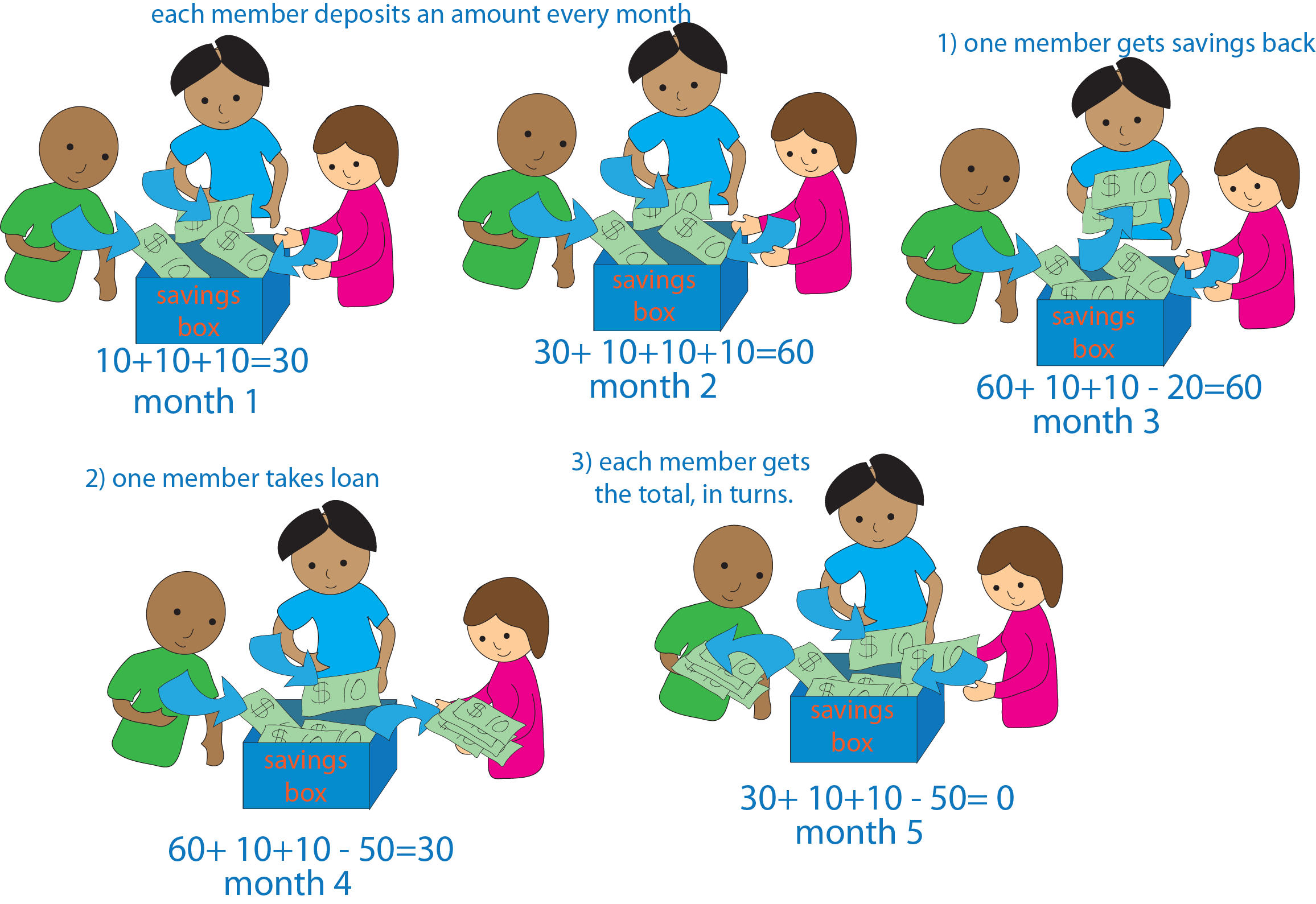

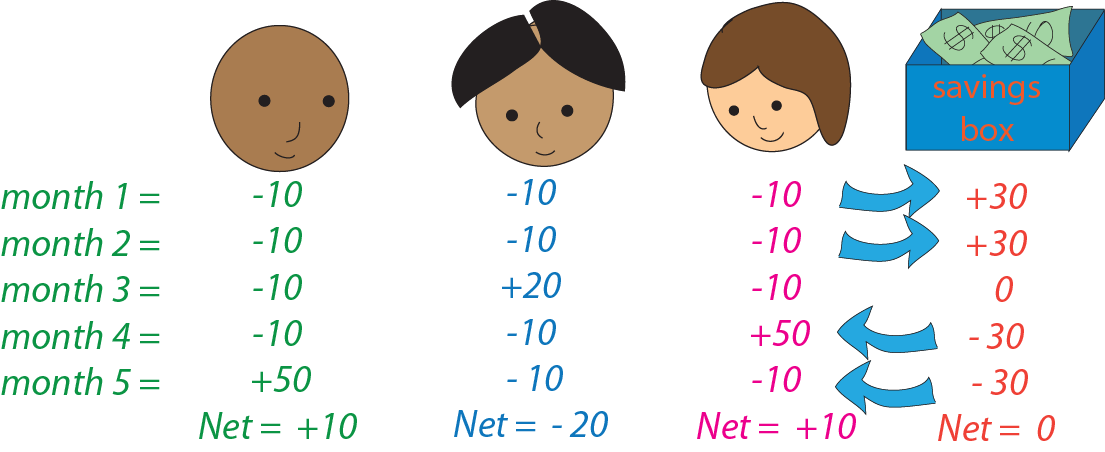

Savings groups (or tontines):

A group of people (neighbours, friends, family, etc.) pool their savings each week or month, usually in a common fund. They then take turns distributing the money from the fund, either as a payment to one of their members or as a loan (often with interest). This is a redistribution of each member’s savings among themselves, according to the rules established by the group. In the case of a loan with interest, the person paying the interest contributes more to the tontine than the others. There is a redistribution of money from borrowers to lenders.

Example (without interest):

Let’s summarise the flows: savings circulate between members of the group:

| Pros | Cons |

|

|

- Check the rules governing the savings group; prefer written rules; assess whether they are actually being implemented.

- Ensure that the records are up-to-date, accurate, and approved by all members.

- If the savings group’s purpose is a specific community project, discuss it and agree on the details.

- Consider depositing group savings using mobile technology and avoid keeping savings in cash.

- Ensure that the account (whether mobile money or bank account) is not in the name of a single person.

- Share the responsibilities (one person keeps the cash, another the key, another the records, etc.) to minimize the risk of embezzlement if one person has all the responsibilities.

- If you have access to banking or mobile money and lack the self-discipline to save, set up an automatic monthly transfer to another (savings) account in your name.

The current (bank) account: (checking account in US)

If you deposit cash into your account, the bank takes the cash and records the deposit, i.e. it credits your account with the same amount in “digital money,” which is the most commonly used type of money. It will use this digital money when other customers (or yourself) make a withdrawal.

If you receive digital money into your account (for example, a salary transfer), the bank credits your account with the amount. The person who initiated the transfer (your employer, for example) has a corresponding entry deducted. This is a system of accounting entries between bank accounts. The value of these entries lies in the fact that banks are legally obligated to convert this digital money into cash. Furthermore, in many countries, the central bank (the bank that oversees all others) is committed to honoring the obligations of a bank that fails: it will pay customers with current accounts up to a certain amount defined by law. In summary, the digital money you have in your bank account is a debt owed to you by the bank.

| Pros | Cons |

|

|

- Check if the bank (or mobile money operator) is officially registered and review its history and reputation.

- Check the fees (on deposits and withdrawals) and the minimum deposit amount. Compare banks.

- Check and keep your bank statements.

- Requires discipline: don’t overdraw your account (if your withdrawals or payments exceed the balance): the bank will charge you very high overdraft fees.

Savings Accounts:

Savings accounts are also bank accounts, but with slightly different operating rules. For example, there may be a higher minimum balance requirement, penalties for frequent withdrawals, or withdrawals before a certain date, and in return, the bank commits to paying interest to the account holder. As with a current account, the bank records a debt in digital money corresponding to the amounts you deposit into your savings account.

But where does the interest come from? Money is a flow: when we receive interest, it means that someone else had to pay extra so that we could receive more than we deposited. The bank uses its income (usually the interest received on the loans it grants) to pay the interest on savings accounts. We will discuss this in more detail in the next lesson.

| Current account | Savings account |

What for ? To manage everyday expenses (bills, etc.). |

What for? To save for goals and try to maintain purchasing power (if the interest rate is higher than inflation or price increases). |