Curriculum

Tips to manage money

Introduction

0/1Part 1: Learn the basics

0/7Part 2: Let's go further

0/6Part 3: the world of finance

0/712. To have or to be: what is wealth?

Have you looked at your bank account? Have you checked the conditions and how much bank fees you pay? Is it in line with what you need? Are you getting more interested in the economic world: do you try to figure out the ins and outs around you? Have you read articles or watched financial news?

Do you remember what money is? It is mostly accounting entries on banks’ books. For our last lesson, it’s time to look at what an accounting entry looks like – that will help you understand more about the world of money… and if you have or plan to have a business, this will be useful to follow its accounts (our next series will be on business!).

Accounting is … story-telling, using a specific language.

What story does it tell? Accounting tells the story of the money flows, who (or where) it comes from and who (or where) it goes to. The source is called debit and the destination is called credit. Because everything is recorded twice (hence the term “double entry accounting”), that helps detect errors: every flow has a beginning and an end, so the total of the beginnings must be equal to the total of the ends.

Did you know?

The first writing system was accounting records in clay balls in Mesopotamia… so accounting can claim to be the most ancient written language!

Do you remember that money is based on trust, and debts create money…

Debit = comes from Latin, debitum = what is due

Credit = comes from Latin, to believe, trust. Creditum = something entrusted (to someone else)

Let’s take an example. The food shop has borrowed 200 from the bank. What do the bank and the shop accountants record?

| Bank: | Shop: | |||

|

Where it comes from |

Where it goes

Credit

|

Where it comes from

Debit |

Where it goes

Credit

|

|

| Loans to customers : 200 | Shop’s account: 200 | Bank account: 200 | Bank loan: 200 |

Have you noticed? The bank’s book is the exact mirror of the shop’s book. Someone’s debt… is someone else’s property. A credit… is money that we have been entrusted with, so we owe it, while a debit is money that is due to us. Wait a minute… when we receive a bank statement, it is the other way round: a debit means less money for us, and a credit means more money. Yes, because a bank statement is an extract of the bank’s book, so a credit means more money in your bank account, which means more money entrusted to the bank.

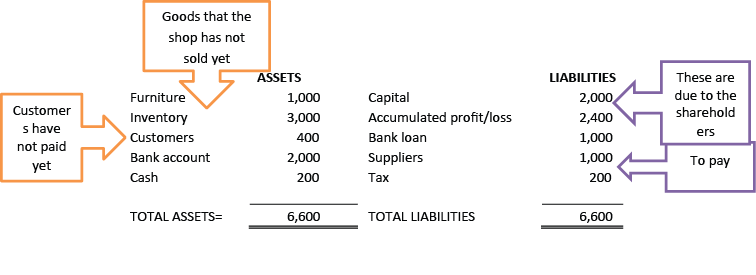

All the debits and credits are recorded… but that can make a long story. So the accountant summarises the story. One of the main summaries is called ‘balance sheet‘: it shows all the money owed to a business (including the other valuables like machines and inventory) and the money a business owes (including to its shareholders or partners). Let’s have a look at one simple balance sheet:

If you cannot see the picture, here is the balance sheet

| ASSETS (=debit) | Amount | LIABILITIES (=credit) | Amount |

| Furniture | 1,000 | Capital | 2,000 |

| Inventory | 3,000 | Accumulated profit/loss | 2,400 |

| Customers | 400 | Bank loan | 1,000 |

| Bank account | 2,000 | Suppliers | 1,000 |

| Cash | 200 | Tax | 200 |

| TOTAL ASSETS | 6,600 | TOTAL LIABILITIES | 6,600 |

The balance sheet tells the story of the business (there are two other useful summaries called “cash flow” and “income statement” that also add up the debits and credits and tell another aspect of the story). By reading a business a balance sheet, you can see if a business is healthy before investing in it (either as partner or as shareholder).

You can do the same and calculate your own ‘balance sheet’ and see how healthy your financial situation is!

Let’s take an example:

| ASSETS | Amount | LIABILITIES | Amoun |

| Cash | 50 | ||

| Bank account | 2,000 | ||

| Savings account | 1,000 | ||

| Main residence | 100,000 | Bank loan | 60,000 |

| Other property, land | 10,000 | ||

| Financial Investments | 5,000 | ||

| Pension plan | 5,000 | ||

| Loans Receivable | 200 | ||

| Valuables (hewels…) | 2,000 | ||

| TOTAL ASSETS | 125,250 | TOTAL LIABILITIES | 60,000 |

| ASSETS – LIABILITIES = | 65,250 |

This personal (family) balance sheet is also called ‘net worth’: it helps you see all that you have minus what you owe. For your financial situation to be “healthy”, you will need:

- a positive ‘net worth’ (more assets than debts)

- a balanced net worth:

Look at this other example:

| ASSETS | Amount | LIABILITIES | Amount |

| Bank account | 200 | Credit card debt | 10,000 |

| House | 1,000,000 | ||

| TOTAL ASSETS | 1,000,200 | TOTAL LIABILITIES | 10,000 |

| ASSETS – LIABILITIES | 990,200 |

The net worth is super positive…but not balanced: debts are very short term… and the assets are all long term. How will this family pay their debt?

What is wealth?

Does the net worth measure how wealthy you are? A net worth measures what you have (net of what you may owe); but is “having” things and money the only wealth? What about health, education, ethics, attitude, character, relationships? What is your goal in life: to grow your “having” or your “being”? To have or to be, this is your choice. Money is part of who we are, of our life; we are not split in two… there is not money on one side and our feelings and emotions on the other. Money is part of us: by using money, we show who we are: generous, careless, thoughtful, foresighted… so work on who you aspire to be, which qualities you want to embody… then align the way you manage money to reflect these qualities. And track your expenses and incomes to check whether you are true to yourself.

Here is a proverb to think about: “The real measure of your wealth is how much you’d be worth if you lost all your money.“

Let’s put this into practice:

- Calculate your net worth:

- You should already have your list of debts (if any) (lesson 3)

- Assets:

- Cash: count it

- Bank accounts: take the balance on your latest bank statement.

- Other financial accounts or investments: you should receive a statement once a year at least that tells you how much they owe you.

- Valuables: like a house, or some collectibles or jewellery: list them and take their market value (how much you would get if you sold them)… by the way, this list will be useful to take or renew your insurance.

- Other expensive valuables like cars, motorbikes, electronic equipment, appliances and furniture… tend to wear out, get damaged and lose value quickly. So only include a realistic market value including their dents, problems, etc…

- Small items… like clothes, pots and pans, crockery, home textiles, books, etc… may not be worth to be included in your calculation… unless you are in an emergency situation and desperate for cash and you need to value how much cash you may get from selling them.

- Update your net worth once or twice a year – when you do your yearly budget for example, or if there is a big change (new debt or lasting valuable purchase).

- Balance your net worth:

- If it is negative: write your budget, re-prioritise expenses so that you can pay back your debts gradually, and avoid taking new ones.

- If debts are very short term but assets are very long term: write your budget, re-prioritise expenses so that you can get out of debt with the money you earn. If this is not enough, consider selling some long term assets.

- Take care of your assets.

- To have or to be… this is your choice: Look at your expenses and flag those that can help you improve your ‘being’ (non-financial wealth) like education, health, ethics…

Ask questions… the forum is open for you for general questions or send us a message!