Curriculum

Tips to manage money

Introduction

0/1Part 1: Learn the basics

0/7Part 2: Let's go further

0/6Part 3: the world of finance

0/711. Banks are for profit businesses

How are you managing your social expenses? Have you clarified any dodgy relationships with friends or relatives?

Today, we’re looking upstream… where does the money come from?... which will allow us to answer this fundamental question: what is money?

Remember (lesson 10): if we were alone, we would not need money; money is a social tool – a tool to interact with others. It is a flow that goes from one person to another. Or like ping pong… have you ever tried to play ping pong alone?

Money has no real value in itself. Money has value only because we can exchange it with other people and get things or services…. It is the way that human societies have chosen (very early on) to organise exchanges and make them easier. Imagine if each of us made our own money… how could we be sure how much our friend’s money is worth, or whether the food shop would accept it? Money has value because others accept it. And they accept our money because they believe it has value: money is all about trust.

Why do we trust money has value? Because as an organised group (= a society), we have set rules (laws) that we all follow. Like… a ping pong game, as a society, we have decided how to play, what size and weight the balls are, how big the table is, etc.… Money is the same: the Government has decided what money to use in the country it governs, who can issue money, etc… . These rules ensure we all trust the money can be used as a tool of exchange.

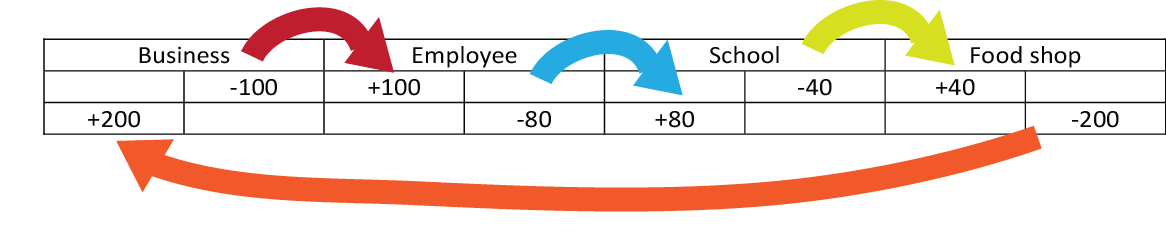

Money is a tool of exchange: someone’s expense is someone else’s income. Let’s take a very simple example with four people only: A Business, an Employee, a School and a Food shop. The Business pays the Employee who pays the School fee and the School buys food for the students from the Food shop that buys more supplies from the Food Business. Let’s look at this ping pong game in slow motion and find out how to play and more importantly… where does the first player pick up the ball from?

1) The Business pays the Employee.

How does the money ball bounce from the Business to the Employee? On the table… banks are the tables enabling balls to bounce from one player to the other. This is their first role: they manage the payment system. How does it work?

Two learning points from this example:

Two learning points from this example:

- Banks pay one another every day (the ins minus the outs from their various customers’ transactions, as well as loans to one another) through their accounts (also called reserves) at the Central Bank (the bank of banks).

- Money… is mostly digital numbers in computers, i.e. accounting records in the banks’ books. Cash is only a small part of the money. We’ll see why in a few minutes.

2) The Employee pays the school fee.

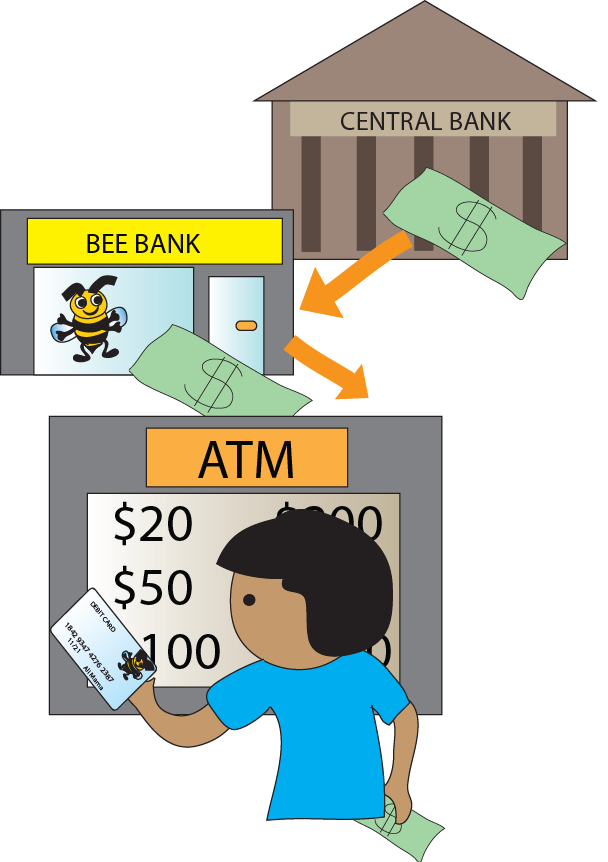

Slow motion again: the Employee goes to the bank and withdraws 80 from his bank account. Banks keep some cash for their customers to withdraw, but this cash does not generate any income for the banks, so they only keep the amount of cash that they think customers will need, not more. Where do banks get this cash? From the Central Bank. So that gives one answer to our question (where does the ping pong ball come from?). Cash is created by the Central Bank. (NB: in some countries, the Central Bank is ruled by the Government; in other countries, the Central Bank is independent from the Government.)

Question: Could the Central Bank or the Government print as much cash as it wants? … It could but it would have serious side effects: imagine if there were too many ping pong balls on the tables! Trust would go down … the value of the balls would go down (or balls would be smaller). So if the business sells a box of biscuits for 2 ping pong balls… and a ping pong ball is worth less, it will sell the box for 3 ping pong balls. In financial terms, if the money is worth less, it often drives prices up (inflation). The second impact would be on the exchange rate (the price of one country’s money compared to the price of another country’s money): the new smaller balls would be exchanged for more of the other country’s balls.

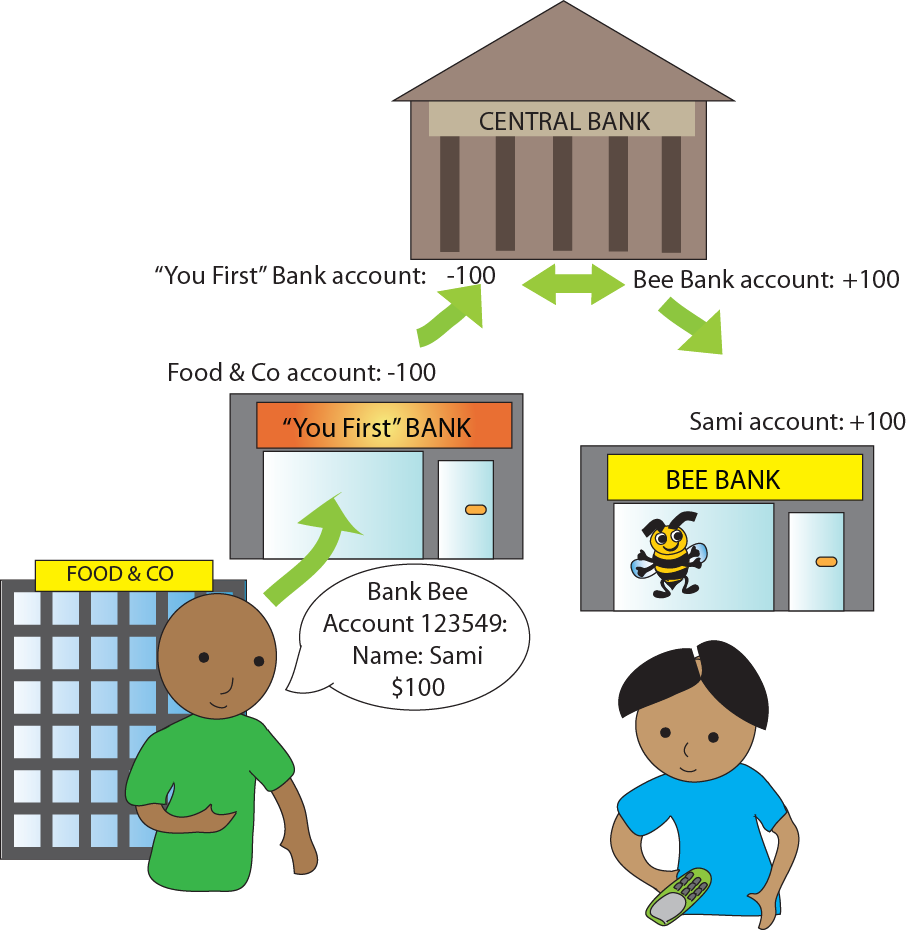

3) The school pays the shop.

The school pays cash, and the shop deposits the cash to its bank account.

Practically the bank takes the cash, records the deposit in its books as a debt towards the shop, and puts the cash into its cash box. If another customer comes to withdraw cash, the bank will take from the same cash box to hand him cash. Or this cash can also be used to fill in the ATM. At the end of the day, all the cash is counted and reconciled and if the bank estimates it is too much, it can deposit it to the Central Bank… or if it is not enough (before a big Holiday like New Year for example), it may ask the Central Bank for more (for example, if Bank Bee has 1000 on its reserve at the Central Bank, it can ask 400 in cash, so its reserve becomes 600 in digital money, and 400 in cash).

Another learning point from this example: someone’s debt… is someone else’s property. Or in finance word, someone’s liability (=debt) is someone else’s asset (=property). When we deposit money to the bank, the bank records a debt to us. And when we borrow money from the bank, the bank has a financial asset (we owe the bank).

4) The shop buys supply from the business.

The shop orders more goods from the business… but it has not enough money and decides to take a bank loan. (*) Let’s go in super slow motion – this is for most countries the main way that nowadays money is created (more balls are added to the ping pong game):

The bank considers whether the shop is creditworthy… can it trust the shop to pay back in time? To do so, it will look at its credit rating (how has the shop repaid its debts in the past?). If it agrees to lend money, the bank takes its books and records two things:

- “Shop” owes us 200;

- “Shop” has now 200 in its bank account.

By lending money, the bank has created a deposit… i.e. money: loans create money. And in many economies, this is the main way that money is created, by commercial banks.

(*) Another way the shop could pay would be to negotiate a credit with the business, i.e. pay the business 30 or 60 days for example after the delivery of the goods. By that time, the shop will have sold the goods, get money from its customers and be able to pay the business. It would be cheaper (no interest)… but as everything in economics and business, it depends on trust (does the business trust the shop and is ready to grant a credit) and on relation and negotiation (is the shop a customer that the business values?).

Let’s zoom on commercial banks: We have learned so far that:

- Banks manage the payment system (they are the tables on which ping pong balls bounce).

- Banks provide most of the balls… by lending them. Loans create deposits and deposits are money.

- Banks are businesses: their goal is to make profit. They charge fees on their services (especially for the use of the payment system), and they charge interest on loans, which is higher than the interest they may pay on the deposits (the difference between the two interests is called ‘spread’).

Remember in lesson 11 we asked where the interest could come from: the interest is an extra payment… so it requires extra money to be created. We now know how most money is created: by loans; new loans make deposits that pay for the interest.

Another way is to make the circle wider and transform natural resources (for example, exporting minerals to another country that will pay in money), or services which were free, into money. Money may be digital or virtual but it impacts the real world!

Key learning points:

- Someone’s expense is someone else’s income.

- Someone’s debt… is someone else’s property.

- Money is a social tool of exchange and its value depends on the trust of those who use it.

- Practically, money has two main forms (*): cash (less and less) and accounting numbers in computers (more and more) (for example in UK, bank deposits are 97% of the total money vs. 3% in cash).

- Banks don’t take cash deposited from customers to lend it to other customers. It’s the other way round: bank lends money, and these loans create the deposits. So loans create money, and when loans are paid back, money is destroyed. However interest stays; it is a transfer of income from the borrower to the bank and has to come from somewhere else.

- Banks make profit by lending at a higher interest rate than they may give on deposits.

- Learn more on economics: how money is allocated among the various ‘players’, how this has an impact on jobs, the environment, how financial decisions are connected to the tangible world, what taxes are used for, etc…

(*) the third form is the Central Bank money (reserves), used by banks to pay each other.

Let’s put this into practice:

Commercial banks are for profit businesses. Their income… is our expense. Our debts… is their property… and our deposits are their debts to us.

- Be clear: you can’t get what you need… if you don’t know what you need. So do your budget and find out how much you plan to deposit and maintain on your bank account, what payment services you need, etc; this will help you find what bank services are the best fit for you… you buy clothes that fit you, don’t you?

- Inquire and compare: get detailed information on the fees applicable to current accounts, transactions, ATM withdrawals, minimum deposits, papers and conditions to open an account, or borrow money, convenience (location, opening hours, branches network….), etc… Compare several banks and make an educated decision.

- Before signing anything, ask for the contract and read the fine lines. Or ask someone trustworthy to read them to you.

- Resist pressure to buy a financial service 1) you don’t need (see point 1 on being clear) or 2) you don’t understand.

- Ask questions when things are not clear. There is no dumb question.

- Prepare your appointment with a banker. Whether you meet a banker to open an account, save or borrow, prepare what you need (budget), and list your questions (for loans for instance, do they ask for a collateral, what is the loan schedule, are there penalties to pay back in advance, etc…).

- Track: bank fees and interests in separate categories in your tracking… and see how much they add up at the end of the year.

- Optimise: choose your payment types, account… in order to lower the fees you have to pay (unless a higher fee…also means less time spent).

- Check and keep: your bank statements, fees, etc… mistakes can happen. Behind computers, there are real humans! This will also help reduce the fees!

Let’s take an example of decision making. You have opened a bank account and the bank offers you a debit card to go with it.

- Ask questions: Is the debit card free? Do you charge a withdrawal fee each time I withdraw cash from an ATM?

- Get clear answers: The card is not free: there is a 10 fee to pay once a year. There is a 1 withdrawal fee if you withdraw cash from an ATM which is outside our network; here is the list of the nearest ATM in our network.

- Compare

Choices Pros Cons Get card Quicker (no queue at bank), open 24 hours a day, can withdraw smaller amount more often, several ATMs near my home. Pay 10 a year

Pay 1 if I use an ATM outside their network

Don’t get card save 10 a year Will take more cash each time I go to the bank > more risk to … spend it! Or get stolen or lost. Get card from other bank lower fee, several ATMs near my home Hassle (paper work, time to go to new bank and open new account…)

Smaller overall network

Fee on all withdrawals - Weigh the pros and cons and decide More risks… to spend the money if I carry lots of cash. Safer to keep more in bank – this is worth paying the 10 fee.

Are all banks for profit? No, there are several types of financial institutions; what they are allowed to do, and how they work depends on each country’s law. In many countries, credit or savings unions (also called cooperatives or mutual) offer a different model: their customers are also the owners (shareholders) of the union/cooperative, so their fees and operating mode reflect this.

Money is virtual… but consequences are real. Weigh the pros and cons before deciding!